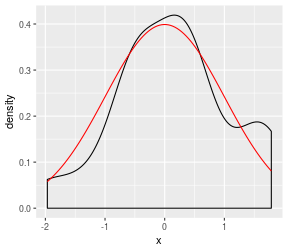

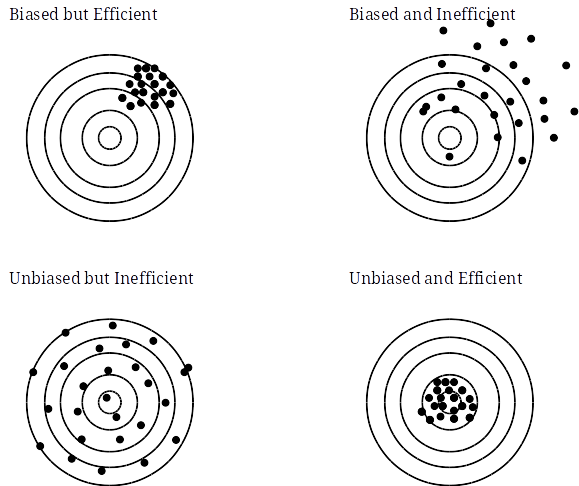

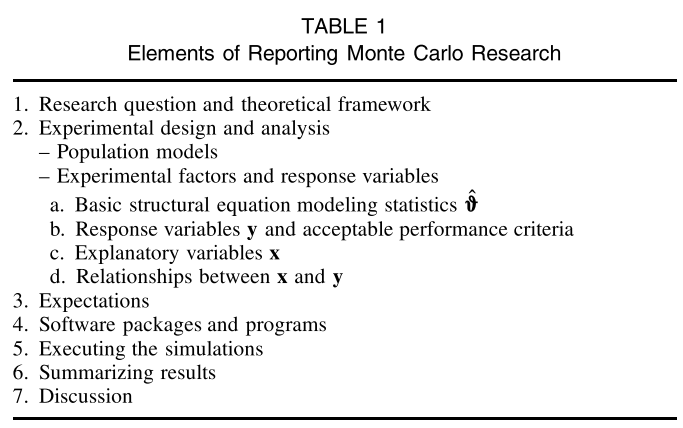

class: center, middle, inverse, title-slide # Advancing Quantitative Science ## with Monte Carlo Simulation <html> <div style="float:left"> </div> <hr color='#EB811B' size=1px width=796px> </html> ### Hok Chio (Mark) Lai ### 2019/05/16 --- # Monte Carlo Methods .pull-left[ - 1930s-1940s: Nuclear physics * Key figures: * Stanislaw Ulam * John von Neumann * Nicholas Metropolis * Manhattan project: hydrogen bomb - Naming: Casino in Monaco ] .pull-right[  ] --- # Why Do We Do Statistics? - To study some target quantities in the population * Based on a limited sample - How do we know that a statistics/statistical method gets us to a reasonable answer? * Analytic reasoning * Simulation --- class: inverse, center, middle # MC is one way to understand the properties of one or more statistical procedures --- # What is MC (in Statistics)? - Simulate the _process of repeated random sampling_ * E.g., repeatedly drawing sample of IQ scores of size 10 from a population - Approximate _sampling distributions_ * Using __pseudorandom samples__ - Study properties of __estimators__ * regression coefficients, fit index * compare multiple estimators or modeling approaches --- # What is it (cont'd)? - Based on Carsey & Harden (2014): * Simulations as experiments * Whether there's a "treatment" effect (but not why) * Simulations help develop intuition * Shouldn't replace analytically and theoretical reasoning * Simulations help evaluate substantive theories and empirical results ??? Sometimes analytic solution does not exist --- # Examples in the Literature - [Curran, West, & Finch (1996, Psych Methods)](http://dx.doi.org/10.1037/1082-989X.1.1.16) studied the performance of the `\(\chi^2\)` test for nonnormal data in CFA - [Kim & Millsap (2014, MBR)](http://dx.doi.org/10.1080/00273171.2014.947352) studied the performance of the Bollen-Stine Bootstrapping method for evaluating SEM fit indices - [MacCallum, Widaman, Zhang, & Hong (1999, Psych Methods)](http://dx.doi.org/10.1037/1082-989X.4.1.84) studied sample size requirement for getting stable EFA results - [Maas & Hox (2005, Methodology)](http://dx.doi.org/10.1027/1614-2241.1.3.86) studied the sample size requirement for multilevel models --- # Generating Random Data in R With MC, one simulates the process of generating the data with an assumed __data generating model__ - Model: including both functional form and distributional assumptions .font80[ ```r rnorm(5, mean = 0, sd = 1) ``` ``` ## [1] 0.8863733 1.6361050 -1.3694538 -1.1621330 1.1365392 ``` ```r rnorm(5, mean = 0, sd = 1) # number changed ``` ``` ## [1] 0.6607360 -0.7283291 0.5751322 1.4180376 -1.5442535 ``` ] --- # Setting the Seed - Most programs use algorithms to generate numbers that look like random * _pseudorandom_ * Completely determined by the _seed_ - For replicability, <font color="red">__ALWAYS__</font> explicitly set the seed in the beginning .font80[ ```r set.seed(1) rnorm(5, mean = 0, sd = 1) ``` ``` ## [1] -0.6264538 0.1836433 -0.8356286 1.5952808 0.3295078 ``` ```r set.seed(1) rnorm(5, mean = 0, sd = 1) # same seed, same number ``` ``` ## [1] -0.6264538 0.1836433 -0.8356286 1.5952808 0.3295078 ``` ] --- # Generating Data From Univariate Distributions ```r rnorm(n, mean, sd) # Normal distribution (mean and SD) runif(n, min, max) # Uniform distribution (minimum and maximum) rchisq(n, df) # Chi-squared distribution (degrees of freedom) rbinom(n, size, prob) # Binomial distribution ``` ??? Other distributions include `exponential`, `gamma`, `beta`, `t`, `F` --- # MC Approximation of `\(\mathcal{N}(0, 1)\)` .small[ ```r library(tidyverse) set.seed(123) nsim <- 20 # 20 samples sam <- rnorm(nsim) # default is mean = 0 and sd = 1 ggplot(tibble(x = sam), aes(x = x)) + geom_density(bw = "SJ") + stat_function(fun = dnorm, col = "red") # overlay normal curve in red ``` <!-- --> ] --- class: inverse # Exercise Try increasing `nsim` to 100, then 1,000 --- # Exercise  --- # Parameter vs Estimator - __Estimator__/statistic: `\(T(\mathbf{X})\)`, or simply `\(T\)` * How good does it estimate the population parameter, `\(\theta\)`? - Examples: * `\(T = \bar{X}\)` estimates `\(\theta = \mu\)` * `\(T = \dfrac{\sum_i (X_i - \bar{X})^2}{N - 1}\)` estimates `\(\theta = \sigma^2\)` --- # Properties of Estimators - Bias - Consistency - Efficiency - Robustness --- # What is a Good Estimator?  --- # Sampling Distribution - What is it? <!-- --> --- class: inverse, center, middle # Example I Simulating Means and Medians --- # When to use MC? - When it's difficult to analytically derive the sampling distribution * E.g., indirect effect, fit-indexes; Cohen's `\(d\)`, *SE*s of estimators - When required assumptions are violated * E.g., normality, large sample * Model is misspecified * Used to check __robustness__ of the estimator --- # A Simulation Study is an Experiment Experiment | Simulation -----------|------------ Independent variables | Design factors Experimental conditions | Simulation conditions Controlled variables | Other parameters Procedure/Manipulation | Data generating model Dependent variables | Evaluation criteria Substantive theory | Statistical theory Participants | Replications --- class: clear, center <img src="images/Sigal&Chalmers_figure1.png" width="65%" /> (Sigal and Chalmers, 2016, Figure 1, p. 141) --- # Design Like experimental designs, conditions should be carefully chosen - What to manipulate? Sample size? Effect size? Why? * Based on statistical theory and reasoning * E.g., Gauss-Markov theorem: regression coefficients are unbiased with violations of distributional assumptions - What levels? Why? * Needs to be realistic for empirical research * Maybe based on previous systematic reviews, * Or a small review of your own --- # Design (cont'd) Full Factorial designs are most commonly used Other alternatives include fractional factorial, random levels, etc - See Skrondal (2000) for why they should be used more often --- # Generate - Starts with a statistical data generating model * E.g., `\(Y_i = \beta_0 + \beta_1 X_i + e_i,\quad e_i \overset{\textrm{i.i.d.}}{\sim} N(0, \sigma^2)\)` + Systematic (deterministic) component: `\(X_i\)` + Random (stochastic) component: `\(e_i\)` + Constants (parameters): `\(\beta_0\)`, `\(\beta_1\)` * `\(Y_i\)` completely determined by `\(X_i, e_i, \beta_0, \beta_1\)` <div id="htmlwidget-daf636270d129b757355" style="width:504px;height:252px;" class="grViz html-widget"></div> <script type="application/json" data-for="htmlwidget-daf636270d129b757355">{"x":{"diagram":"\ndigraph reg {\n\n # a \"graph\" statement\n graph [overlap = true, fontsize = 10]\n\n # several \"node\" statements\n node [shape = box,\n fontname = Helvetica]\n X; Y\n\n node [shape = circle,\n fixedsize = true] // sets as circles\n e\n\n # several \"edge\" statements\n X -> Y\n e -> Y\n {rank = same; X; Y;}\n}\n","config":{"engine":"dot","options":null}},"evals":[],"jsHooks":[]}</script> --- # Model-Based Simulation <img src="images/sampdist2.png" width="75%" /> --- # Analyze Analyze the simulated data using one or more analytic approaches - Misspecification: study the impact when analytic model omits important aspects of data generating model * E.g., ignoring clustering - Comparison of approaches * E.g., Maximum likelihood vs. multiple imputation for missing data handling --- # Summarize (Evaluation Criteria) - `\(\bar{\hat \theta}\)` = `\(\sum_{i = 1}^R \hat \theta_i / R\)` - `\(\hat{\mathit{SD}}(\hat \theta)\)` = `\(\sqrt{\frac{\sum_{i = 1}^R (\theta_i - \bar{\hat \theta})^2}{R}}\)` For evaluating estimators: - Bias * Raw: `\(\bar{\hat \theta} - \theta\)` * Relative: Bias / `\(\theta\)` * Standardized: Bias / `\(\hat{\mathit{SD}}(\hat \theta)\)` - Relative efficiency (only for unbiased estimators) * `\(\mathrm{RE}(\hat \theta, \tilde \theta)\)` = `\(\frac{\hat{\mathrm{Var}}(\tilde \theta)}{\hat{\mathrm{Var}}(\hat \theta)}\)` --- # Evaluation Criteria (cont'd) For uncertainty estimators - SE bias * Raw: `\(\overline{\mathit{SE}(\hat \theta)} - \hat{\mathit{SD}}(\hat \theta)\)` * Relative: SE bias / `\(\hat{\mathit{SD}}(\hat \theta)\)` Combining bias and efficiency - Mean squared error (MSE): `\(\frac{\sum_{i = 1}^R (\theta_i - \theta)^2}{R}\)` * Also = `\(\mathrm{Bias}^2 + \hat{\mathrm{Var}}(\hat \theta)\)` * Root MSE (RMSE) = `\(\sqrt{\mathrm{MSE}}\)` - Mainly to compare 2+ estimators --- # Evaluation Criteria (cont'd) For statistical inferences: - Power/Empirical Type I error rates * % with `\(p < \alpha\)` (usually `\(\alpha\)` = .05) - Coverage of `\(C\)`% CI (e.g., `\(C\)` = 95%) * % where the sample CI contains `\(\theta\)` --- class: clear .font80[ Criterion | Cutoff | Citation -----|-------|---------- Bias |.|. Relative bias | ≤5% | Hoogland and Boomsma (1998) Standardized bias | ≤.40 | Collins, Schafer, and Kam (2001) *SE* bias |.|. Relative *SE* bias | ≤10% | Hoogland and Boomsma (1998) MSE |.|. RMSE |.|. Empirical Type I error (α = .05) | 2.5% - 7.5% | Bradley (1978) Power |.|. 95% CI Coverage | 91%-98% | Muthén and Muthén (2002) ] --- # Results Just like you're analyzing real data - Plots, figures - ANOVA, regression * E.g., 3 (sample size) × 4 (parameter values) 2 (models) design: 2 between factors and 1 within factor --- class: inverse, center, middle # Example II Simulation Example on Structural Equation Modeling --- # Number of Replications Should be justified rather than relying on rule of thumbs ## Why Does MC Work? - Law of large number * `\(\sum_{i = 1}^R T_i / R \overset{p}{\to} \theta\)` - When `\(R\)` is large, + the empirical distribution `\(\hat{F}(t)\)` converges to the true sampling distribution `\(F(t)\)`. --- # Number of Replications (cont'd) ## How Good is the Approximation - Monte Carlo (MC) Error * Like standard error (SE) for a point estimate - For expectations (e.g., bias) * MC Error = `\(\hat{\mathit{SD}}(\hat \theta) / \sqrt{R}\)` E.g., if one wants the MC error to be ≤2.5% of the sampling variability, _R_ needs to be 1 / `\(.025^2\)` = 1,600 --- # Number of Replications (cont'd) For power (also Type I error) and CI coverage, * MC Error = `\(\sqrt{\frac{p (1 - p)}{R}}\)` E.g., with _R_ = 250, and empirical Type I error = 5%, ```r sqrt((.05 * (1 - .05)) / 250) ``` ``` ## [1] 0.01378405 ``` So _R_ should be increase for more precise estimates --- # Reporting MC Results  (Boomsma, 2013, Table 1, p. 521) See Boomsma (2013), Table 2, p. 526 for a checklist --- # Efficiency tips - Things that don't change should be outside of a loop - Initialize place holders when using for-loops - [Vectorize](https://adv-r.hadley.nz/perf-improve.html#vectorise) - Strip out unnecessary computations - Parallel computing (using the `future` package) --- # Other topics not covered - Error handling - Assessing convergence - Debugging - Interfacing with other software (e.g., Mplus, LISREL, HLM) --- # Further Readings Carsey and Harden (2014) for a gentle introduction Chalmers (2019) and Sigal and Chalmers (2016) for using the R package `SimDesign` Harwell, Kohli, and Peralta-Torres (2018) for a review of design and reporting practices Skrondal (2000), Serlin (2000), and Bandalos and Leite (2013) for additional topics --- class: inverse, center, middle # Thanks! --- # References .font70[ Bandalos, D. L. and W. Leite (2013). "Use of Monte Carlo studies in structural equation modeling research". In: _Structural equation modeling. A second course_. Ed. by G. R. Hancock and R. O. Mueller. 2nd ed. Charlotte, NC: Information Age, pp. 625-666. Boomsma, A. (2013). "Reporting Monte Carlo studies in structural equation modeling". In: _Structural Equation Modeling_. _A Multidisciplinary Journal_ 20, pp. 518-540. DOI: [10.1080/10705511.2013.797839](https://doi.org/10.1080%2F10705511.2013.797839). Bradley, J. V. (1978). "Robustness?" In: _British Journal of Mathematical and Statistical Psychology_ 31, pp. 144-152. DOI: [10.1111/j.2044-8317.1978.tb00581.x](https://doi.org/10.1111%2Fj.2044-8317.1978.tb00581.x). Carsey, T. M. and J. J. Harden (2014). _Monte Carlo Simulation and resampling. Methods for social science_. Thousand Oaks, CA: Sage. Chalmers, P. (2019). _SimDesign: Structure for Organizing Monte Carlo Simulation Designs_. R package version 1.13. URL: [https://CRAN.R-project.org/package=SimDesign](https://CRAN.R-project.org/package=SimDesign). ] --- # References (cont'd) .font70[ Collins, L. M, J. L. Schafer, and C. Kam (2001). "A comparison of inclusive and restrictive strategies in modern missing data procedures". In: _Psychological Methods_ 6, pp. 330-351. DOI: [10.1037//1082-989X.6.4.330](https://doi.org/10.1037%2F%2F1082-989X.6.4.330). Harwell, M, N. Kohli, and Y. Peralta-Torres (2018). "A survey of reporting practices of computer simulation studies in statistical research". In: _The American Statistician_ 72, pp. 321-327. ISSN: 0003-1305. DOI: [10.1080/00031305.2017.1342692](https://doi.org/10.1080%2F00031305.2017.1342692). Hoogland, J. J. and A. Boomsma (1998). "Robustness studies in covariance structure modeling". In: _Sociological Methods & Research_ 26, pp. 329-367. DOI: [10.1177/0049124198026003003](https://doi.org/10.1177%2F0049124198026003003). Muthén, L. K. and B. O. Muthén (2002). "How to use a Monte Carlo study to decide on sample size and determine power". In: _Structural Equation Modeling_ 9, pp. 599-620. DOI: [10.1207/S15328007SEM0904_8](https://doi.org/10.1207%2FS15328007SEM0904_8). Serlin, R. C. (2000). "Testing for robustness in Monte Carlo studies". In: _Psychological Methods_ 5, pp. 230-240. DOI: [10.1037//1082-989X.5.2.230](https://doi.org/10.1037%2F%2F1082-989X.5.2.230). ] --- # References (cont'd) .font70[ Sigal, M. J. and R. P. Chalmers (2016). "Play it again: Teaching statistics with Monte Carlo simulation". In: _Journal of Statistics Education_ 24.3, pp. 136-156. ISSN: 1069-1898. DOI: [10.1080/10691898.2016.1246953](https://doi.org/10.1080%2F10691898.2016.1246953). URL: [https://doi.org/10.1080/10691898.2016.1246953 https://www.tandfonline.com/doi/full/10.1080/10691898.2016.1246953](https://doi.org/10.1080/10691898.2016.1246953 https://www.tandfonline.com/doi/full/10.1080/10691898.2016.1246953). Skrondal, A. (2000). "Design and analysis of Monte Carlo experiments". In: _Multivariate Behavioral Research_ 35, pp. 137-167. DOI: [10.1207/S15327906MBR3502_1](https://doi.org/10.1207%2FS15327906MBR3502_1). ]